Fill Out Your Rpd 41359 New Mexico Form

The RPD-41359 form plays a crucial role for Pass-Through Entities (PTEs) and their owners in New Mexico, guiding them through the process of reporting and withholding state tax on net income. Revised on August 27, 2014, by the New Mexico Taxation and Revenue Department, this form is designed to ensure that all parties comply with the Oil and Gas Proceeds and Pass-Through Entity Withholding Tax Act. It offers a structured way for entities to report New Mexico net income and state tax withheld for each owner. Owners, including partners, members, and beneficiaries, are then required to attach this form, or its alternatives like Form 1099-MISC, to their New Mexico state income tax return to claim the income and tax withheld. The detailed instructions differentiate between requirements for PTEs and those for owners, making it clear how to complete and submit the necessary documentation by the specified deadlines. This form not only facilitates compliance with state taxation laws but also aids owners in accurately claiming their income and withheld taxes, emphasizing the importance of timely and correct filing to both parties.

Rpd 41359 New Mexico Sample

New Mexico Taxation and Revenue Department

Annual Statement of

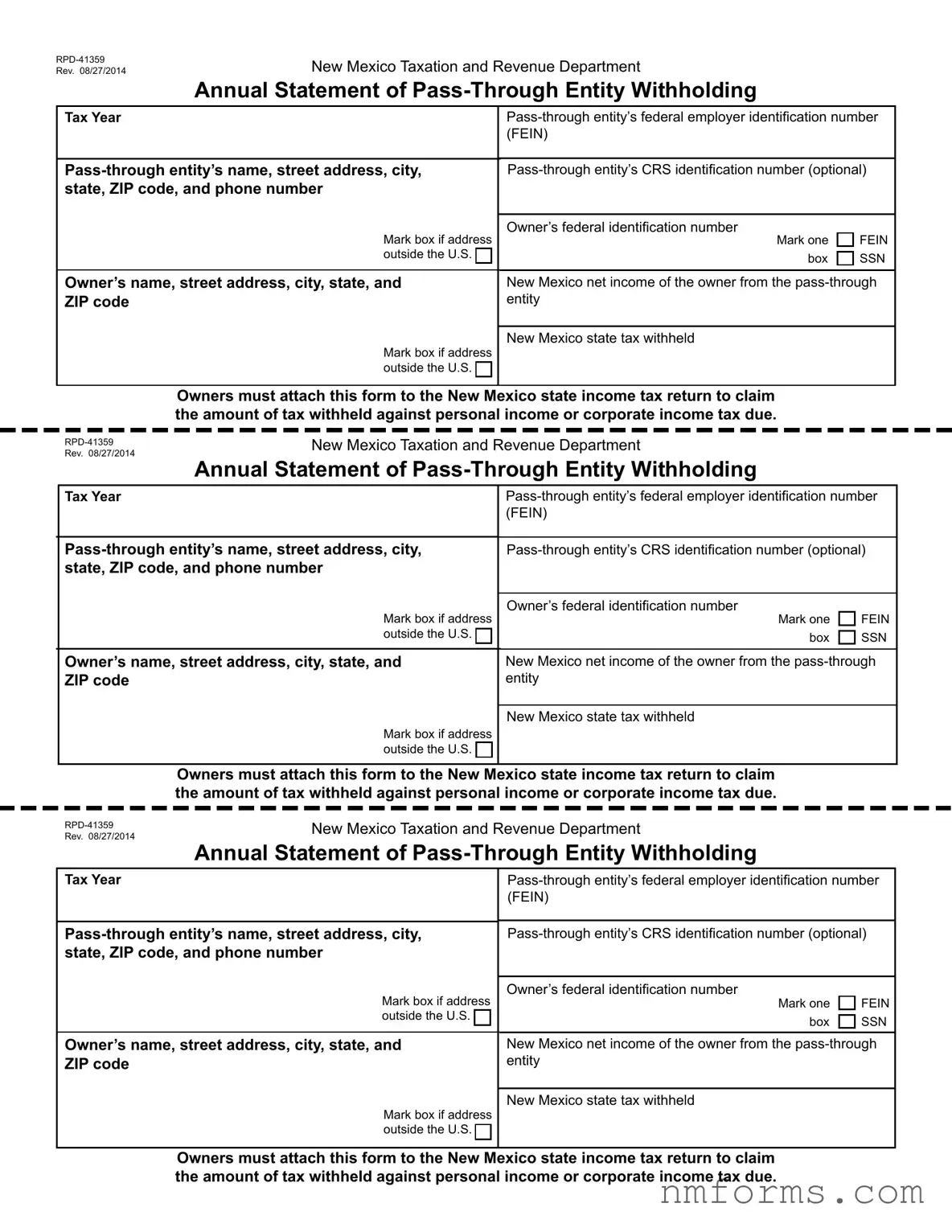

Tax Year |

|||

|

(FEIN) |

|

|

|

|

||

state, ZIP code, and phone number |

|

|

|

|

|

|

|

Mark box if address |

Owner’s federal identiication number |

Mark one |

FEIN |

outside the U.S. |

|

box |

SSN |

|

|

||

|

|

||

Owner’s name, street address, city, state, and |

New Mexico net income of the owner from the |

||

ZIP code |

entity |

|

|

|

|

|

|

Mark box if address |

New Mexico state tax withheld |

|

|

|

|

|

|

outside the U.S. |

|

|

|

|

|

|

|

Owners must attach this form to the New Mexico state income tax return to claim the amount of tax withheld against personal income or corporate income tax due.

New Mexico Taxation and Revenue Department

Annual Statement of

|

Tax Year |

||

|

|

(FEIN) |

|

|

|

|

|

|

|||

|

state, ZIP code, and phone number |

|

|

|

|

|

|

|

Mark box if address |

Owner’s federal identiication number |

|

|

Mark one |

FEIN |

|

|

outside the U.S. |

box |

SSN |

|

Owner’s name, street address, city, state, and |

New Mexico net income of the owner from the |

|

|

ZIP code |

entity |

|

|

|

|

|

|

|

New Mexico state tax withheld |

|

|

Mark box if address |

|

|

|

outside the U.S. |

|

|

|

|

|

|

Owners must attach this form to the New Mexico state income tax return to claim the amount of tax withheld against personal income or corporate income tax due.

New Mexico Taxation and Revenue Department

Annual Statement of

Tax Year |

|

||

|

|

(FEIN) |

|

|

|

|

|

|

|||

state, ZIP code, and phone number |

|

|

|

|

|

|

|

Mark box if address |

|

Owner’s federal identiication number |

|

|

Mark one |

FEIN |

|

outside the U.S. |

|

box |

SSN |

|

|

||

Owner’s name, street address, city, state, and |

|

New Mexico net income of the owner from the |

|

ZIP code |

|

entity |

|

|

|

|

|

Mark box if address |

|

New Mexico state tax withheld |

|

|

|

|

|

outside the U.S. |

|

|

|

|

|

|

|

Owners must attach this form to the New Mexico state income tax return to claim the amount of tax withheld against personal income or corporate income tax due.

New Mexico Taxation and Revenue Department

Annual Statement of

Instructions

page 1 of 2

About This Form.

cording to the Oil and Gas Proceeds and

NMSA 1978), are required to annually submit

Annual Statement of

use any of these three forms) to owners.

Owners (including partners, members, and beneiciaries,

which are all considered owners) must attach the forms received from PTEs to their New Mexico state income tax returnstoclaimtheamountofincomeandtaxwithheldagainst their personal income or corporate income tax due.

IMPORTANT: If no owners received net income from the

PTE for a calendar year, no ilings are required for that year.

An estate or trust that distributes New Mexico net income that is taxable to its recipients is a PTE and subject to

withholding pursuant to the Oil and Gas Proceeds and Pass- Through Entity Withholding Tax Act (Sections

An entity that has had tax withheld cannot pass a withholding statement directly to another taxpayer. Generally, the recipi- ent of the withholding statement must ile and report the tax

withheld on its New Mexico income tax return.

For Help. To get help with this form and corporate income taxes, in Santa Fe call (505)

help@state.nm.us.

INSTRUCTIONS FOR

This section is for PTEs. If you are an owner, see page 2,

Instructions for Owners.

What to File. To report the New Mexico net income and the state tax withheld for each owner, you are required to ile

Department and one of these forms to owners (any of these forms is acceptable):

•New Mexico Form

•Form

•A pro forma Form

If the net income you paid on Form

income from New Mexico and the amount of New Mexico tax withheld.

Other Reporting Requirements. PTEs are required to pro- vide suficient information to enable owners to comply with the

provisions of the Income Tax Act and the Corporate Income

and Franchise Tax Act, with respect to an owner’s share of

the net New Mexico income. A PTE that uses a Schedule

•New Mexico Form

•Form

•A pro forma Form

Due Date to Send Forms to Owners. Send the forms

the year for which you withheld New Mexico state tax from their net income. If February 15 falls on a Saturday, Sunday, or a state or national legal holiday, the return is timely if the postmark bears the date of the next business day.

How to Complete

Column 1

Year and Contact Information

1.Enter the tax year.

2.Enter your PTE name, address, and phone number. If the address is outside the U.S., mark the box.

3.Enter the owner’s name and address. If the address is outside the U.S., mark the box.

Column 2

Identiication Numbers, Net Income, and State Tax Withheld

1.Enter your PTE federal employer identiication number

(FEIN) using hyphens in

2.If applicable, enter the owner’s Combined Reporting System (CRS) identiication number using hyphens in

3.Enter the owner’s federal identiication number using hy- phens. If the number is an FEIN, enter it in

4.Enter the New Mexico net income the PTE allocated to the owner.

5.Enter the New Mexico state tax withheld.

New Mexico Taxation and Revenue Department

Annual Statement of

Instructions

page 2 of 2

Send Each Owner a Copy. After completing

(or Form

ForMoreInformation.See

INSTRUCTIONS FOR OWNERS

This section is for owners. If you are a PTE, see page 1,

Instructions for

Due Date to File with the State. You are required to ile the

How to File. Attach

income tax return when claiming the New Mexico income and the amount of tax withheld against your personal or corporate income tax due.

IMPORTANT:Unless you are listed as the owner or the recipi- ent of the income, do not attach these forms to your income tax return. When iling your return, you cannot use an income

and withholding statement that is issued to someone else.

File Specifics

| Fact | Detail |

|---|---|

| Title of Form | Annual Statement of Pass-Through Entity Withholding |

| Form Number | RPD-41359 |

| Revision Date | 08/27/2014 |

| Governing Law | Oil and Gas Proceeds and Pass-Through Entity Withholding Tax Act (Sections 7-3A-1 through 7-3A-9 NMSA 1978) |

| Purpose | To report and withhold New Mexico tax from each owner's share of net income allocable to New Mexico |

| Applicability | Pass-through entities (PTEs) and their owners, including partners, members, and beneficiaries |

| Requirement for Owners | Owners must attach this form to their New Mexico state income tax return to claim the withheld tax amount |

| Filing Requirement for No Income | If no owners received net income from the PTE for a calendar year, no filings are required for that year |

| Due Date for PTEs | Forms must be sent to owners by February 15 of the following year |

| Contact Information for Help | In Santa Fe call (505) 827-0825, toll free (866) 809-2335 and select option 4, or email cit.taxreturn-help@state.nm.us |

How to Use Rpd 41359 New Mexico

The RPD-41359 form is an essential document for those navigating the intricacies of tax obligations for pass-through entities in New Mexico. This mandatory submission plays a crucial part in ensuring that tax withheld from each owner's share of net income is correctly accounted for and claimed on personal or corporate tax returns. To navigate this form properly, a detailed, step-by-step guide can help demystify the process, paving the way for accuracy in reporting and compliance with state tax regulations.

Steps to Fill Out the RPD-41359 New Mexico Form

- Begin by entering the tax year for which the withholding is being reported at the top of the form.

- Write the Pass-through entity’s name, complete street address, city, state, ZIP code, and phone number in the designated space. If the entity's address is outside the United States, remember to mark the corresponding box.

- Provide the Pass-through entity’s federal employer identification number (FEIN), placing hyphens appropriately in the XX-XXXXXXX format.

- If applicable, enter the Pass-through entity’s CRS identification number, including hyphens in the designated format of XX-XXXXXX-XXX. Note that this step is optional.

- Next, detail the Owner’s federal identification number, ensuring to use hyphens for the proper format. Specify by marking whether it’s an FEIN (XX-XXXXXXX) or SSN (XXX-XX-XXXX).

- Fill in the Owner’s name, complete street address, city, state, and ZIP code. Mark the appropriate box if the owner's address is outside the U.S.

- Record the New Mexico net income of the owner from the pass-through entity, ensuring accuracy as this will impact tax obligations.

- Input the New Mexico state tax withheld amount, which is crucial for the owner to claim against their tax due.

- Upon completing the form, it is essential to send each owner a copy by February 15 following the year for which the tax was withheld. If February 15 falls on a weekend or legal holiday, ensure the form is postmarked by the next business day.

Following these steps meticulously ensures compliance with New Mexico's tax reporting requirements for pass-through entities and their owners. Proper completion and timely submission of the RPD-41359 form provide a foundation for accurate tax reporting and facilitate the correct claiming of tax credits or withheld amounts against personal or corporate income tax due. It is critical to retain a copy of this form for records, alongside any other tax documentation, to support the accuracy of submitted financial information.

Understanding Rpd 41359 New Mexico

-

What is the RPD-41359 form used for in New Mexico?

The RPD-41359 form, known as the Annual Statement of Pass-Through Entity Withholding, is used by pass-through entities (PTEs) to report and withhold New Mexico tax from each owner's share of net income that is allocable to New Mexico. This form helps to detail the income distributed and tax withheld for each owner, and it must be filed annually with the New Mexico Taxation and Revenue Department. Owners, including partners, members, and beneficiaries, must attach the forms they receive from PTEs to their New Mexico state income tax returns to claim the amount of income and tax withheld against their personal income or corporate income tax due.

-

Who needs to file the RPD-41359 form?

Any pass-through entity (such as partnerships, S corporations, fiduciaries for estates, and trusts) that allocates net income to its owners derived from New Mexico sources and is required to withhold New Mexico state tax on that income needs to file the RPD-41359 form. Additionally, an estate or trust distributing New Mexico net income taxable to its recipients as a PTE is also obligated to withhold and submit this form to the Taxation and Revenue Department.

-

What are the deadlines for submitting the RPD-41359 form and distributing copies to owners?

PTEs must send the completed RPD-41359 form, or its alternatives like Form 1099-MISC or a pro forma Form 1099-MISC, to their owners by February 15 of the year following the year in which New Mexico state tax was withheld from their net income. If February 15 falls on a weekend or a state or national holiday, the forms are timely if postmarked by the next business day.

-

How can an owner of a pass-through entity use the RPD-41359 form?

Owners of pass-through entities must attach the RPD-41359 form, or an acceptable alternative like Form 1099-MISC or pro forma Form 1099-MISC, to their New Mexico state income tax return. This form is crucial for owners to claim the New Mexico income and the amount of state tax withheld against their tax obligations. Important to note, the form should only be filed with the state if it directly pertains to the individual or entity filing the return; it cannot be used if it is issued to another party.

Common mistakes

Not using the correct Federal Employer Identification Number (FEIN) format: Many individuals mistakenly enter the FEIN without the required hyphens (XX-XXXXXXX). This common error can lead to processing delays or even form rejection.

Omitting the Combined Reporting System (CRS) identification number: While the CRS number is optional, failing to include it when it is applicable can prevent accurate processing of the form, especially for entities that have multiple reporting requirements.

Incorrectly marking the FEIN or SSN box for the owner’s federal identification number: It is crucial to mark the correct box to indicate whether the number provided is a FEIN or a Social Security Number (SSN). This mistake can cause confusion and inaccuracies in tax reporting and withholding information.

Leaving the New Mexico net income of the owner from the pass-through entity blank: Some filers forget to report the New Mexico net income allocated to the owner. This is essential information for accurately calculating the tax obligation.

Failing to adequately mark the box if the address is outside the U.S.: For both the entity’s and the owner’s addresses, it's important to indicate if the address is outside the United States. This detail affects how the form is processed and ensures compliance with international mailing requirements.

Not attaching the form to the New Mexico state income tax return: Owners must attach this form to their New Mexico state income tax return to claim the tax withheld. Overlooking this step can result in the loss of the ability to claim the withheld amount against their tax due.

Remember: Carefully reviewing and accurately completing all sections of the RPD-41359 form ensures timely and correct processing of your tax information. Avoid common mistakes by double-checking the form before submission and ensuring that all necessary attachments are included.

Documents used along the form

When dealing with tax documents and compliance for pass-through entities (PTEs) in New Mexico, particularly with the usage of the RPD-41359 form, it's essential to recognize the variety of other documents and forms that are often required or used alongside. These documents play a critical role in ensuring the accurate reporting and withholding of taxes, as well as compliance with state taxation laws.

- PTE Declaration of Estimated Income Tax (RPD-41272): This form is used by pass-through entities to declare and pay estimated income tax in New Mexico. It ensures compliance with tax payment schedules throughout the fiscal year.

- Annual Withholding Tax Reconciliation Statement (RPD-41072): This form is designed for entities to reconcile the taxes withheld from employees or other payees throughout the tax year with the actual taxes owed.

- Composite Tax Return (RPD-41368): Filed by the pass-through entity on behalf of non-resident owners, this return simplifies the tax reporting and payment process by allowing a collective filing.

- Application for Extension of Time to File (RPD-41096): If a pass-through entity needs additional time to prepare their annual filing, this document can be filed to request an extension.

- Schedule K-1: Used to report each shareholder or partner's share of income, deductions, credits, etc., Schedule K-1 ensures that the tax responsibilities are accurately reported to individual owners.

- Form 1099-MISC: This form reports miscellaneous income. While it is federally mandated, it is also pertinent for states like New Mexico for reporting certain types of income not covered by traditional wage reports.

- Form CRS-1: The Combined Reporting System (CRS) form for New Mexico is used by businesses to report gross receipts tax, compensating tax, and withholding tax.

- Application for Registration (ACD-31015): This form is required for new businesses or entities in New Mexico to register for tax purposes, including acquiring a CRS identification number.

- Oil and Gas Proceeds Withholding Tax Return (RPD-41285): For entities involved in the oil and gas sector, this return specifically addresses the withholding requirements associated with proceeds from this industry.

Together, these forms and documents complement the RPD-41359 by ensuring a holistic approach to tax compliance. Whether it's dealing with estimated taxes, reconciling withholdings, or satisfying industry-specific tax requirements, these documents facilitate a comprehensive and compliant tax reporting process for pass-through entities in New Mexico.

Similar forms

The RPD-41359 New Mexico form is similar to other documents designed for tax reporting and compliance. Each document has specific applications, but they all facilitate the reporting of income and tax withholding for different entities and individuals. Below, we address how the RPD-41359 form compares to similar documents regarding their format, purpose, and the information required.

Firstly, the RPD-41359 form shares similarities with the Form 1099-MISC. Both documents are utilized for reporting income and tax withholdings to the tax authorities. While the RPD-41359 is specifically tailored for pass-through entities reporting in New Mexico, the 1099-MISC has a broader application, used across the United States by businesses to report payments made to non-employees, such as independent contractors. The key similarity lies in their function of reporting income to the authorities and the individual or entity receiving the income. However, the RPD-41359 zooms in on the reporting requirements for pass-through entities and their owners within New Mexico, emphasizing state tax withholdings.

Another comparable document is the Schedule K-1. This form is part of the IRS Form 1065 and is used to report individual partners' share of a partnership's earnings, deductions, credits, etc. Like the RPD-41359, the Schedule K-1 focuses on pass-through entities, but it goes beyond just reporting income and withholdings. It provides a detailed breakdown of various components of the partner's taxable income from the entity. The similarity lies in their shared goal of reporting pass-through entity activities to individual members or partners, aiding them in accurately filing their tax returns with detailed information about their share of the entity's financial activities.

Dos and Don'ts

Filling out the RPD-41359 New Mexico form can seem a bit daunting, but knowing what to do and what not to do can simplify the process. Below are some guidelines to follow when completing this form:

Do:

- Double-check the tax year and all contact information entered, ensuring accuracy for both the pass-through entity and the owner.

- Use hyphens appropriately when entering federal employer identification numbers (FEIN) and social security numbers (SSN) to comply with the required format.

- Clearly mark the correct boxes indicating if any addresses are outside the U.S., as this can affect the form's processing.

- Include the correct New Mexico net income allocated to the owner, as well as the state tax withheld, to accurately report income and withholdings.

Don't:

- Overlook the deadline for sending forms to owners, which is February 15 of the year following the year for which New Mexico state tax was withheld from their net income.

- Forget to provide sufficient information to enable owners to comply with the provisions of the Income Tax Act and the Corporate Income and Franchise Tax Act regarding their share of the net New Mexico income.

- Mix up the types of identification numbers (FEIN vs. SSN) or forget to mark the corresponding box, as this could cause issues with processing the form.

- Fail to attach this form to the New Mexico state income tax return if you're an owner claiming the amount of tax withheld against personal or corporate income tax due.

Adhering to these dos and don'ts can help avoid common mistakes and ensure that the RPD-41359 New Mexico form is filled out correctly and efficiently.

Misconceptions

Many people have misconceptions about the RPD-41359 form in New Mexico, which can lead to confusion or misunderstandings regarding its use and requirements. Here are seven common misconceptions and the truths behind them:

- It's only for residents. Some may think that the RPD-41359 form is only for New Mexico residents. However, this form is crucial for both residents and non-residents who receive income through pass-through entities in New Mexico. It helps them claim state tax withheld on their income tax returns.

- It replaces the need for a 1099-MISC form. Another misconception is that filing the RPD-41359 negates the need for a 1099-MISC form. While similar in purpose, these forms serve different functions and may both be required from pass-through entities, depending on the specific circumstances and the types of income being reported.

- Submission is optional. Some people incorrectly believe submitting this form is optional. In fact, pass-through entities are required to submit the RPD-41359 or an equivalent form annually if they withhold New Mexico tax from each owner’s share of net income.

- It's only for reporting net income. The form is not solely for reporting the pass-through entity's net income to the owner. It also reports the New Mexico state tax withheld from that income, which is crucial for owners to claim against their tax due.

- Direct submission to the New Mexico Taxation and Revenue Department is unnecessary. Actually, the entity must file this form with the New Mexico Taxation and Revenue Department and also provide a copy to the owners. It's an essential step for both compliance and for owners to claim their tax withholdings.

- It includes federal income and tax withheld. Some might misunderstand that this form reports on federal income and tax withheld as well. However, the form specifically addresses income and taxes related to the state of New Mexico only.

- The form can be substituted with any withholding statement. While the RPD-41359 form, Form 1099-MISC, or a pro forma Form 1099-MISC can be used to report to owners, simply substituting it with any withholding statement disregards New Mexico Taxation and Revenue Department's specific requirements. One of these designated forms must be used to properly report the necessary information.

Understanding these key points about the RPD-41359 form helps in ensuring compliance and accurate tax reporting for entities and individuals navigating New Mexico's tax obligations related to pass-through income.

Key takeaways

Here are key takeaways about properly filling out and using the RPD-41359 New Mexico form, which is essential for pass-through entities and their owners within New Mexico:

- Pass-through entities (PTEs) in New Mexico must annually submit the RPD-41359 form, or a Form 1099-MISC, to report and withhold state taxes from each owner’s share of net income allocable to New Mexico.

- This form is required by the Oil and Gas Proceeds and Pass-Through Entity Withholding Tax Act (Sections 7-3A-1 through 7-3A-9 NMSA 1978).

- Owners, including partners, members, and beneficiaries, should attach the form they received from the PTE to their New Mexico state income tax returns to claim the amount of income and tax withheld.

- In situations where no owners received net income from the PTE for a given calendar year, no filings are necessitated for that year.

- Trusts or estates distributing New Mexico net income taxable to its recipients are deemed PTEs and thus are obligated to withhold for the non-resident recipient’s share of taxable New Mexico net income.

- PTEs are tasked with providing sufficient information to owners enabling them to comply with the Income Tax Act and the Corporate Income and Franchise Tax Act for their share of net New Mexico income.

- It's a necessity for PTEs to send the completed forms (RPD-41359, Form 1099-MISC, or a pro forma Form 1099-MISC) to their owners by February 15 of the year following which the New Mexico state tax was withheld from their net income. If February 15 falls on a weekend or public holiday, the next business day is considered the due date.

- To complete the RPD-41359 form, enter the tax year, pass-through entity (PTE) name, address, phone number, and Federal Employer Identification Number (FEIN), along with the owner’s name, address, and either their FEIN or Social Security Number (SSN).

- The Owners of the Pass-Through Entities must file the RPD-41359, Form 1099-MISC, or pro forma Form 1099-MISC alongside their New Mexico state income tax return by the due date of their tax return to properly claim the tax withheld.

These guidelines aim to facilitate compliance with New Mexico's taxation requirements for both pass-through entities and their respective owners, ensuring the proper withholding and reporting of state taxes.

Other PDF Forms

Nm Courts Forms - Highlights the essential elements of a civil claim, including the specific events or transactions leading to the legal action.

New Mexico State Tax Return - Details about the corporation's fiscal year, state of incorporation, and the date business began in New Mexico are required.

Refund Money Application - This versatile form accommodates refund requests for miscellaneous errors in payments made to the New Mexico Motor Vehicle Division.