Fill Out Your New Mexico Pit Rc Form

The 2013 PIT-RC New Mexico Rebate and Credit Schedule offers a detailed framework for individuals seeking to claim refundable rebates and credits on their New Mexico Personal Income Tax Return. With its inclusion alongside Form PIT-1, the schedule is designed to ensure taxpayers who meet specific criteria related to income levels, residency, and personal circumstances can navigate the process of securing their entitled financial benefits efficiently. Covering a broad spectrum of rebates including those for property taxes, child day care expenses, and low-income comprehensive tax rebates, the PIT-RC form requires thorough completion of sections that examine qualifications, calculate allowable household members and modified gross income. Additionally, it extends to more unique credits like the refundable medical care credit for persons 65 or older, special needs adopted child tax credit, and renewable energy production tax credit. By following the detailed instructions and accurately reporting income and exemptions, eligible individuals and families in New Mexico can potentially reduce their tax liability, thereby reinforcing the state's commitment to assisting its residents in various financial landscapes.

New Mexico Pit Rc Sample

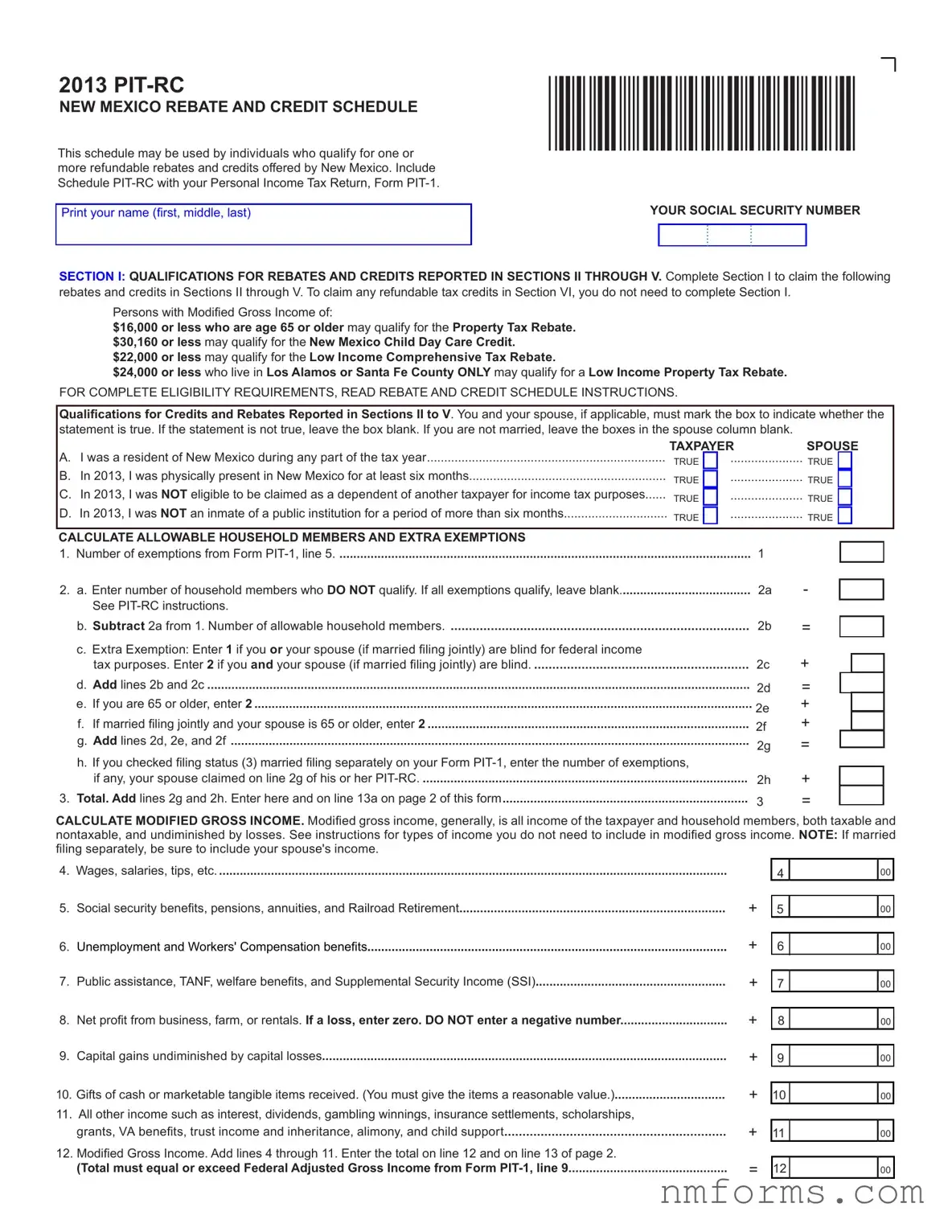

2013

NEW MEXICO REBATE AND CREDIT SCHEDULE

This schedule may be used by individuals who qualify for one or more refundable rebates and credits offered by New Mexico. Include Schedule

Print your name (irst, middle, last)

*130380200*

YOUR SOCIAL SECURITY NUMBER

SECTION I: QUALIFICATIONS FOR REBATES AND CREDITS REPORTED IN SECTIONS II THROUGH V. Complete Section I to claim the following rebates and credits in Sections II through V. To claim any refundable tax credits in Section VI, you do not need to complete Section I.

Persons with Modiied Gross Income of:

$16,000 or less who are age 65 or older may qualify for the Property Tax Rebate. $30,160 or less may qualify for the New Mexico Child Day Care Credit. $22,000 or less may qualify for the Low Income Comprehensive Tax Rebate.

$24,000 or less who live in Los Alamos or Santa Fe County ONLY may qualify for a Low Income Property Tax Rebate.

FOR COMPLETE ELIGIBILITY REQUIREMENTS, READ REBATE AND CREDIT SCHEDULE INSTRUCTIONS.

Qualiications for Credits and Rebates Reported in Sections II to V. You and your spouse, if applicable, must mark the box to indicate whether the statement is true. If the statement is not true, leave the box blank. If you are not married, leave the boxes in the spouse column blank.

A. I was a resident of New Mexico during any part of the tax year |

TAXPAYER |

SPOUSE |

||||

TRUE |

..................... TRUE |

|||||

B. In 2013, I was physically present in New Mexico for at least six months |

TRUE |

..................... TRUE |

||||

C. In 2013, I was NOT eligible to be claimed as a dependent of another taxpayer for income tax purposes |

TRUE |

..................... TRUE |

||||

D. In 2013, I was NOT an inmate of a public institution for a period of more than six months |

TRUE |

..................... TRUE |

||||

CALCULATE ALLOWABLE HOUSEHOLD MEMBERS AND EXTRA EXEMPTIONS |

|

|

|

|

|

|

1. |

Number of exemptions from Form |

1 |

|

|

|

|

2. |

a. Enter number of household members who DO NOT qualify. If all exemptions qualify, leave blank |

2a |

- |

|

|

|

|

|

|||||

|

See |

|

|

|

|

|

b. Subtract 2a from 1. Number of allowable household members |

2b |

c. Extra Exemption: Enter 1 if you or your spouse (if married iling jointly) are blind for federal income |

|

tax purposes. Enter 2 if you and your spouse (if married iling jointly) are blind |

2c |

d. Add lines 2b and 2c |

2d |

e. If you are 65 or older, enter 2 |

2e |

|

|

f. If married iling jointly and your spouse is 65 or older, enter 2 |

2f |

g. Add lines 2d, 2e, and 2f |

2g |

|

|

h. If you checked iling status (3) married iling separately on your Form |

|

if any, your spouse claimed on line 2g of his or her |

2h |

3. Total. Add lines 2g and 2h. Enter here and on line 13a on page 2 of this form |

3 |

=

+

=

+

+

=

+

=

CALCULATE MODIFIED GROSS INCOME. Modiied gross income, generally, is all income of the taxpayer and household members, both taxable and nontaxable, and undiminished by losses. See instructions for types of income you do not need to include in modiied gross income. NOTE: If married iling separately, be sure to include your spouse's income.

4. |

Wages, salaries, tips, etc |

|

5. |

Social security beneits, pensions, annuities, and Railroad Retirement |

+ |

6. |

Unemployment and Workers' Compensation beneits |

+ |

7. |

Public assistance, TANF, welfare beneits, and Supplemental Security Income (SSI) |

+ |

8. |

Net proit from business, farm, or rentals. If a loss, enter zero. DO NOT enter a negative number |

+ |

9. |

Capital gains undiminished by capital losses |

+ |

10. Gifts of cash or marketable tangible items received. (You must give the items a reasonable value.) |

+ |

|

11. All other income such as interest, dividends, gambling winnings, insurance settlements, scholarships, |

|

|

|

grants, VA beneits, trust income and inheritance, alimony, and child support |

+ |

12. |

Modiied Gross Income. Add lines 4 through 11. Enter the total on line 12 and on line 13 of page 2. |

|

|

(Total must equal or exceed Federal Adjusted Gross Income from Form |

= |

4 |

|

00 |

|

|

|

|

|

5 |

|

00 |

|

|

|

|

|

6 |

|

00 |

|

|

|

|

|

7 |

|

00 |

|

|

|

|

|

8 |

|

00 |

|

|

|

|

|

9 |

|

00 |

|

|

|

|

|

10 |

|

00 |

|

|

|

|

|

11 |

|

00 |

|

|

|

|

|

|

12 |

|

00 |

|

|

|

|

2013 |

*130390200* |

||

|

|||

NEW MEXICO REBATE AND CREDIT SCHEDULE |

|

||

YOUR SOCIAL SECURITY NUMBER |

|

||

|

|

|

|

|

|

|

|

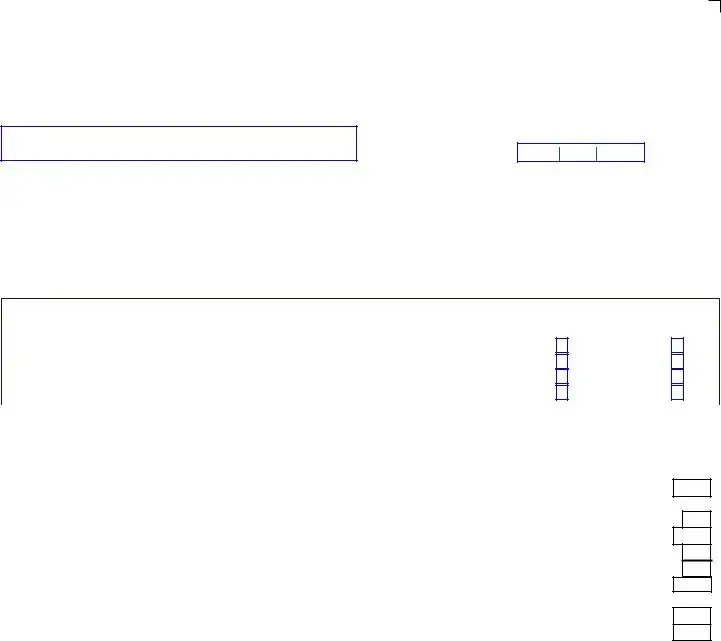

SECTION II: LOW INCOME COMPREHENSIVE TAX REBATE (If line 13 is MORE than $22,000, DO NOT complete line 14.)

13.Enter Modiied Gross Income from line 12 ...............................................................................................................................

a. Enter Total Exemptions from line 3......................................................................................................................................

14.Low Income Comprehensive Tax Rebate. On Table 1 in the instructions, ind the Modiied Gross Income range that includes the amount on line 13, then move across to the column that matches the number of exemptions on

line 13a. Married couples iling separately must divide the result by two. .............................................................................

SECTION III: PROPERTY TAX REBATE FOR PERSONS 65 OR OLDER. (If line 13 is more than $16,000, DO NOT complete this section.)

15.PROPERTY OWNED. Tax billed for the calendar year on principal place of residence

16.PROPERTY RENTED

a. Amount of rent paid during the tax year for principal place of residence .......................................................................................................................................

b. If the amount entered on line 16a includes rent a government entity paid on your behalf, mark here |

16b |

c.Multiply line 16a by 0.06 and enter the amount here ....................................................................................................................

17.REBATE AMOUNT

a.Add lines 15 and 16c and then enter the total here............................................................................................................

b.Find the Modiied Gross Income range, on Table 2 in the instructions, that corresponds to the amount on line 13. Read across the table to the column showing your maximum property tax liability and enter the amount here.................

c.Property Tax Rebate. Subtract line 17b from 17a.

Do not enter more than $250 or if married iling separately, more than $125 ..............................................................................

SECTION IV: ADDITIONAL LOW INCOME PROPERTY TAX REBATE for Los Alamos or Santa Fe County |

18.LA |

|

residents only. (If line 13 is over $24,000, DO NOT complete this section.) |

||

18.SF |

18.REBATE AMOUNT

a.PROPERTY OWNED only. Tax billed for the calendar year on principal place of residence.............................................

b.Find the Modiied Gross Income range, on Table 3 in the instructions, that corresponds to the amount on line 13. Read across the table to the column showing your property tax rebate percentage and enter here..................................

c. Multiply line 18a by line 18b and enter here.

Do not enter more than $350 or if married iling separately, more than $175 .....................................................................

SECTION V: NEW MEXICO CHILD DAY CARE CREDIT. If Modiied Gross Income on line 13 is $30,160 or less, use the worksheet in the instructions to calculate your available Child Day Care Credit. Attach the worksheet and Forms

19. Enter either the total of Column G on the worksheet or $1,200, WHICHEVER IS LESS ........................................................

13 |

|

|

00 |

|

|

|

|

|

|

|

|

13a |

|

|

|

|

|

|

|

14 |

|

|

00 |

|

15 |

|

|

00 |

||||

|

|

|

|

|

|

|

|

16a |

|

|

00 |

||||

|

|

|

|

|

|

|

|

|

16c |

|

|

|

00 |

||

|

|

|

|

|

|

|

|

|

17a |

|

|

|

00 |

||

|

|

|

|

|

|

|

|

17b |

|

|

00 |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

17c |

|

|

00 |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18a |

|

|

|

00 |

|

|

|

|

|

|

|

18b |

% |

|

|

|

|

|

|

18c |

|

|

00 |

|

19 |

|

00 |

20. |

Number of qualiied dependents under age 15 receiving child day care |

20 |

21. |

Enter the portion of the Federal Child Care Credit applied against your federal tax from Form 1040 or 1040A |

21 |

22. |

New Mexico child day care credit. Subtract line 21 from line 19. |

|

|

Married couples iling separately must divide the result by two |

22 |

SECTION VI: REFUNDABLE TAX CREDITS. |

|

|

23. |

Refundable medical care credit for persons 65 or older. See |

23 |

00

00

00

24.Special needs adopted child tax credit.........................................................................................................................

25.Renewable energy production tax credit. Attach Form

26.Refundable portion of the ilm production tax credit. Attach Form

SECTION VII: TOTAL REBATES AND CREDITS CLAIMED.

27. Add lines 14, 17c, 18c, 22, 23, 24, 25, and 26. Enter here and on Form

24

25

26

27

00

00

00

00

File Specifics

| Fact Name | Description |

|---|---|

| Purpose of Form PIT-RC | This form is used by individuals in New Mexico who qualify for one or more refundable rebates and credits. |

| Attachment Requirement | Schedule PIT-RC must be included with the Personal Income Tax Return, Form PIT-1. |

| Qualification Criteria | The form outlines eligibility for various benefits based on age, income, and residency requirements. |

| Special Rebates and Credits | Eligible rebates include Property Tax Rebate, New Mexico Child Day Care Credit, and Low Income Comprehensive Tax Rebate, among others. |

| Modified Gross Income Calculation | Applicants must calculate their modified gross income, which includes all taxable and nontaxable income, to determine eligibility. |

| Governing Laws | These rebates and credits are governed by New Mexico state tax laws and regulations. |

How to Use New Mexico Pit Rc

Filling out the New Mexico PIT-RC form is a process that allows individuals to claim various rebates and credits that New Mexico offers. This form is a crucial component for those who are eligible, as it can significantly affect their personal income tax returns. With a step-by-step guide, the process becomes more manageable, ensuring that all individuals can accurately complete the form and take advantage of the potential financial benefits.

- Begin by printing your name and social security number at the top of the form.

- In Section I, check the appropriate boxes to indicate your eligibility based on residence, physical presence in New Mexico, dependency status, and incarceration.

- For the allowances in Section I, input the number of exemptions from your Form PIT-1, line 5, in the first field (1).

- Determine and enter the number of household members who do not qualify in 2a. If all qualify, leave this blank.

- Calculate the number of allowable household members by subtracting line 2a from line 1 and enter this in 2b.

- If applicable, enter extra exemptions for blindness in field 2c, as per the instructions provided on the form.

- Add the numbers from lines 2b and 2c; then include adjustments for age in lines 2e and 2f. Sum these up in line 2g.

- If you are married filing separately, include your spouse's exemptions if claimed in their PIT-RC on line 2h.

- Total the allowances and exemptions in Section I by adding lines 2g and 2h, placing the result in line 3.

- Proceed to calculate Modified Gross Income (MGI) from lines 4 to 11 by entering the respective amounts for wages, benefits, and other incomes. Add these to get your total MGI in line 12.

- Select your county of residence if you live in Los Alamos or Santa Fe County.

- Based on your modified gross income and other qualifications, proceed to fill out Sections II through VI as applicable, following guidance for each specific rebate or credit.

- For each relevant section, accurately fill in the requested information about your income, property taxes, and childcare expenses. Use the worksheets and instructions as necessary to calculate the correct amounts to claim.

- In Section VII, add up all the rebates and credits from the previous sections and enter the total amount in the designated field (27).

- Review the entire form to ensure all information is correct and accurate.

- Attach the completed PIT-RC form to your New Mexico Personal Income Tax Return, Form PIT-1, before submitting it to the state tax authority.

After completing and attaching the New Mexico PIT-RC to your state tax return, ensure you keep copies for your records. Submitting this form can potentially reduce your tax liability or increase your refund, depending on the rebates and credits for which you are eligible. It's part of the broader process of settling your annual tax obligations and maximizing your benefits under New Mexico tax laws.

Understanding New Mexico Pit Rc

Who is eligible to use the 2013 PIT-RC New Mexico Rebate and Credit Schedule?

Individuals can use the 2013 PIT-RC if they qualify for one or more refundable rebates and credits New Mexico offers. Eligibility is based on various factors, such as income level, age, and residency. For instance, seniors aged 65 or older earning $16,000 or less may qualify for the Property Tax Rebate. There are also qualifications for the New Mexico Child Day Care Credit, Low Income Comprehensive Tax Rebate, and specific rebates for residents of Los Alamos or Santa Fe County based on earning $24,000 or less.

How do I determine the number of allowable household members and extra exemptions?

Calculate allowable household members and extra exemptions by starting with the number of exemptions from your PIT-1 form, line 5. Adjust this number by excluding household members who do not qualify, and then add any extra exemptions for blindness or age (65 or older). The final number, which combines allowable household members and extra exemptions based on blindness and age, should be inserted on the relevant line on page 2 of the PIT-RC form.

What income should be included when calculating Modified Gross Income for the PIT-RC Form?

When calculating Modified Gross Income (MGI) for the PIT-RC Form, include all taxable and nontaxable income of the taxpayer and household members. This includes wages, Social Security benefits, unemployment benefits, public assistance, net profit from businesses, capital gains, and other income such as gifts, dividends, and alimony. It's important not to diminish the total by losses, and if you’re married filing separately, remember to include your spouse's income.

Can I claim the New Mexico Child Day Care Credit?

Yes, if your Modified Gross Income (MGI) is $30,160 or less, you may be eligible for the New Mexico Child Day Care Credit. The credit amount is either the total from Column G on the worksheet or $1,200, whichever is less, for qualified dependents under age 15 receiving child day care. The portion of the Federal Child Care Credit applied against your federal tax should also be identified to calculate the final credit amount for New Mexico accurately.

Common mistakes

Filling out the New Mexico PIT-RC form involves careful attention to details to ensure eligibility for the rebates and credits. However, mistakes can occur that may affect the outcome. Here are seven common mistakes people make when completing this form:

- Not fully completing Section I: Section I is crucial for determining eligibility for the rebates and credits in Sections II through V. Failure to accurately complete this part can lead to missed opportunities for rebates and credits.

- Incorrectly reporting Modified Gross Income: Accurately calculating Modified Gross Income (MGI) in the calculation section is essential. Often, individuals either underreport or overreport income by not following the instructions on which types of income should or should not be included.

- Omitting household member information: Forgetting to calculate and include the number of qualifying household members and exemptions can lead to inaccuracies in rebate and credit amounts.

- Misunderstanding residency requirements: The form requires individuals to have been residents of New Mexico for a specific period or for certain parts of the year. Misinterpreting these requirements can lead to incorrect claims.

- Overlooking age and special status qualifications: Credits and rebates have age and special status qualifications, such as being 65 or older or being blind. Failing to indicate these on the form can result in losing out on eligible benefits.

- Incorrectly claiming the rebates for property owned or rented: For the Property Tax Rebate and the Additional Low Income Property Tax Rebate, accurately entering information regarding property ownership or rental expenses is key. A common mistake is inaccurately reporting these amounts or not properly calculating the rebate.

- Not attaching required documentation: For the New Mexico Child Day Care Credit and other specific credits listed in Section VI, failing to attach the necessary worksheets or Forms PIT-CG can result in disqualification or a reduction of the claimed credit.

Avoiding these mistakes requires thorough review and understanding of the instructions provided with the New Mexico PIT-RC form, ensuring that all information is accurately reported, and all necessary documentation is attached.

Documents used along the form

When individuals in New Mexico prepare their tax returns, especially those taking advantage of rebates and credits like those outlined in the 2013 PIT-RC New Mexico Rebate and Credit Schedule, several other documents and forms often come into play. Understanding these associated documents can streamline the process, ensuring taxpayers efficiently claim all eligible benefits while maintaining compliance with state tax laws.

- Form PIT-1 (Personal Income Tax Return): This is the primary tax return form for New Mexico residents, where you report your income, deductions, and tax credits. Schedule PIT-RC is an attachment to this form.

- Form PIT-CG (Child Day Care Credit Worksheet): Used to calculate the New Mexico Child Day Care Credit, this worksheet helps determine the amount you can deduct based on child care expenses for qualified dependents under age 15.

- Form RPD-41227 (Renewable Energy Production Tax Credit): For individuals or businesses investing in renewable energy, this form is necessary to apply for the renewable energy production tax credit mentioned in the PIT-RC Schedule.

- Form RPD-41228 (Film Production Tax Credit): This form is required for claiming the refundable portion of the film production tax credit, a benefit designed to encourage film production within New Mexico.

- Documentation of Rent Paid: For the Property Tax Rebate and the Low Income Property Tax Rebate, proof of rent paid on your principal place of residence is required to establish the rebate amount.

- Proof of Income Documents: W-2 forms, 1099 forms, and other income statements are crucial for accurately calculating modified gross income on the PIT-RC form.

- Property Tax Statements: Homeowners seeking property tax rebates must provide their property tax statements as proof of the tax billed for the calendar year on their principal residence.

- Social Security and Pension Statements: For sections of the PIT-RC that relate to retirement income, Social Security benefit statements and pension statements can be necessary for determining eligibility for certain credits.

- Documentation for Special Needs Adopted Children: For those claiming the special needs adopted child tax credit, documentation verifying the adoption and special needs status of the child is required.

Effectively gathering and preparing these forms and documents can significantly impact the outcome of one's tax return in New Mexico. By approaching tax preparation comprehensively, incorporating both the PIT-RC form and its relevant supplementary documents, taxpayers ensure they are fully leveraging the state's tax benefits available to them. This careful preparation supports accurate reporting and maximizes potential rebates and credits, ultimately benefiting the taxpayer's financial position.

Similar forms

The New Mexico PIT-RC form is similar to other state tax documents designed to handle rebate and credit schedules, particularly those focused on individual and household financial benefits. This document shares common features with forms like the California 540NR Schedule CA, the New York IT-215 Claim for Earned Income Credit, and the Illinois Schedule ICR for Income Tax Credits. Each of these forms is tailored to capture specific financial data from individuals, enabling them to claim various state-specific tax benefits, adjustments, or credits based on their income level, family size, and eligibility for specific tax incentives. The structural design of the New Mexico PIT-RC form, including sections dedicated to different types of rebates and credits, is a common characteristic across these documents, which strive to streamline the process of applying for fiscal benefits.

The California 540NR Schedule CA shares similarities with the New Mexico PIT-RC form, especially in how it adjusts federal income to conform with state-specific taxation rules. Both forms require individuals to recalibrate their federal income information to suit state tax calculations, making them eligible for certain rebates and credits based on their modified income levels. The California form, like its New Mexico counterpart, has sections where taxpayers must add back certain types of income or subtract allowable expenses and exemptions specific to California’s tax law. This adjustment process ensures accurate reflection of an individual's fiscal status for state tax purposes, thereby determining eligibility for various state-offered financial benefits.

The New York IT-215 Claim for Earned Income Credit also shows similarities with the New Mexico PIT-RC form, particularly in their purpose to provide financial relief to eligible individuals and families through credits. Both forms focus on ensuring that individuals who earn low to moderate income can claim credits to reduce their overall tax liability or receive a refund to aid their financial situation. While the New York IT-215 is specifically focused on the Earniknged Income Credit, the New Mexico PIT-RC encompasses a broader range of credits and rebates, including property tax rebates and child day care credits, each tailored to alleviate the financial burdens on qualifying residents.

The Illinois Schedule ICR for Income Tax Credits is another example that parallels the functionality of the New Mexico PIT-RC form. This form serves to consolidate various tax credits for which Illinois residents may be eligible, including those for education, property taxes, and earned income. Like the New Mexico form, Illinois' Schedule ICR requires taxpayers to detail their qualifications for specific credits, apply income and property information accordingly, and calculate the allowable credit amounts to be deducted from their state tax liability or claimed as a refund. Both documents facilitate the process by which individuals apply for and receive state-specific tax reliefs, highlighting the tailored nature of each form to address the unique credits offered by their respective states.

Dos and Don'ts

When preparing the New Mexico PIT-RC form, it is essential to be thorough and accurate to ensure you claim all eligible rebates and credits correctly. Here are some guidelines to follow:

- Do thoroughly read the instructions for each section of the PIT-RC form before filling it out. Understanding the requirements can help you accurately claim what you're eligible for.

- Do verify your eligibility for each credit or rebate by carefully reviewing the qualifications in Section I. This ensures you only claim credits and rebates for which you truly qualify.

- Do include accurate financial information, especially your modified gross income, to determine the correct rebate or credit amounts. This involves carefully calculating income from all sources as detailed in the form instructions.

- Do double-check the calculations for allowable household members and extra exemptions, as these directly impact the rebate and credit amounts you may be eligible to receive.

- Do ensure that all requested documentation, such as Forms PIT-CG for the child day care credit, is attached when required. Missing documentation can lead to processing delays or denials of claimed rebates and credits.

- Do sign and date the form upon completion. An unsigned form is considered incomplete and will not be processed.

- Don't leave any required fields blank. If a section does not apply to you, clearly indicate with a "N/A" or "0," as appropriate, to demonstrate that the section was not overlooked.

- Don't guess on dates or amounts. Use actual figures and dates to ensure accuracy. Estimations can lead to errors in calculating eligibility and amounts for rebates and credits.

- Don't include sensitive information, such as your Social Security Number, on additional documentation unless specifically required. This helps protect your privacy and reduces the risk of identity theft.

- Don't ignore the specific eligibility requirements for each rebate or credit, especially the income thresholds and residency requirements. These criteria are strictly enforced.

- Don't overlook the requirement to file Form PIT-1, the Personal Income Tax Return, with Schedule PIT-RC. The PIT-RC form is a schedule to the main tax return and cannot be filed independently.

- Don't hesitate to seek assistance if you have questions about filling out the form or determining your eligibility for credits and rebates. Misunderstandings can result in underclaiming or erroneously claiming benefits.

Misconceptions

Many individuals have misconceptions about the New Mexico PIT-RC form, which can lead to confusion or incorrect filing. Here are five common misunderstandings and clarifications to help taxpayers accurately navigate their rebate and credit claims.

- Eligibility Based Solely on Age or Income: A common misconception is that eligibility for rebates and credits on the PIT-RC form is solely based on age or income. However, eligibility also depends on residency status, physical presence in New New Mexico, dependency status, and not being an inmate for more than six months in the tax year, among other factors.

- Rebate and Credit Calculation: Some people think that the rebate and credit amount is a flat rate for all who qualify. However, the actual amount varies. It is calculated based on specific criteria such as modified gross income, household size, and in some cases, the amount of rent paid or property tax billed.

- Requirement to Complete Section I for All Rebates and Credits: There's a misbelief that Section I must be completed to claim any rebates and credits. In reality, Section I only needs to be completed for claiming rebates and credits listed in Sections II through V. For refundable tax credits in Section VI, completing Section I is not necessary.

- Inclusion of All Income Types in Modified Gross Income: Another misunderstanding involves the types of income included in modified gross income. Not all income types are considered. The form specifically instructs taxpayers to exclude certain types of income when calculating their modified gross income, emphasizing that it generally includes both taxable and nontaxable income, undiminished by losses.

- Eligibility Automatically Grants Full Rebate or Credit Amounts: Finally, qualifying for a rebate or credit does not necessarily mean receiving the maximum amount possible. The actual amount received is based on a combination of factors tailored to each specific rebate or credit, such as modified gross income and the number of exemptions."

Understanding these aspects of the PIT-RC form can significantly clarify the filing process for New Mexico taxpayers, ensuring they accurately claim and receive the rebates and credits for which they are eligible.

Key takeaways

Filling out the New Mexico PIT-RC, a form for rebate and credit schedule, is an important task for those who qualify for one or more refundable rebates and credits offered by New Mexico. It serves as an attachment to the personal income tax return, Form PIT-1. Here are six key takeaways to guide you through the process:

- The PIT-RC form is exclusively used to claim various refundable rebates and credits, such as property tax rebate for seniors, low income comprehensive tax rebate, child day care credit, and more. It's essential for residents who meet specific criteria based on age, income, and residential conditions.

- Eligibility for these rebates and credits requires meeting specific income thresholds. For instance, individuals aged 65 or older with a modified gross income of $16,000 or less may qualify for the property tax rebate. Other credits have different income limits and are detailed in the form's instructions.

- Qualification for each rebate or credit necessitates the completion of different sections of the form. Section I focuses on qualifications, while subsequent sections—II through VI—detail the calculation for each specific rebate or credit. Accurate and complete filling out of these sections is crucial.

- It's important to calculate the Modified Gross Income (MGI) accurately. This calculation includes all taxable and nontaxable income for the taxpayer and household members, but some exclusions apply. Details for what income to include or exclude are found in the form's instructions.

- The form also requires detailed information on household composition—including exemptions for blindness, age (65 or over), and the number of qualified dependents for specific credits, like the New Mexico Child Day Care Credit. Ensure this information matches what's reported on Form PIT-1.

- Finally, calculation of rebates and credits often involves using tables provided in the instructions to determine the amount based on Modified Gross Income and total exemptions. These calculations vary, whether filing jointly or separately, and it's imperative to follow the instructions closely to ensure correct credit amounts are claimed.

Completing the PIT-RC form with attention to detail can provide significant financial benefits through rebates and credits from the state of New Mexico. It's an advantageous step for eligible individuals and families to reduce their tax liability and receive refunds where applicable.

Other PDF Forms

New Mexico Oversize Permits Login - Mandates explicit route planning information to assess impact and feasibility of the proposed trip.

Refund Money Application - For handling redundant or unnecessary registration fees and stickers for vehicles or vessels, ensuring a refund is processed.

Do You Have to Claim Dependents on W4 - Clarification on the use of Federal Form W-4 for New Mexico withholding purposes following the 2020 form changes, including instructive steps for employees and employers.